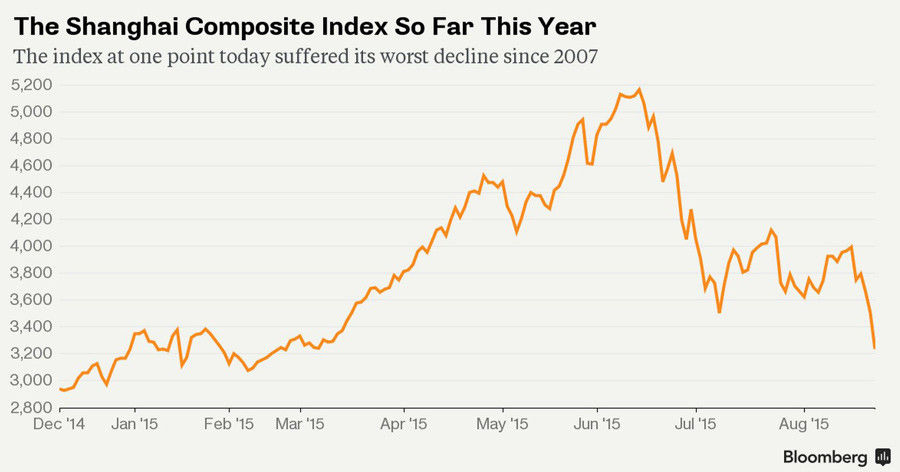

June 12 2015, saw the beginning of the inflated stock market bubble’s collapse, with overvalued stocks being sold en masse, precipitating three consecutive weeks of decline in the Chinese stock market. In the 18 trading days between June 12 and July 8, when the Chinese government implemented a financial rescue package, $3.25 trillion USD was wiped off the Shanghai Composite Index. To place this loss in context, the entire economy of Eurozone member Greece is worth just $237 billion USD.

Beijing’s rescue package involved injecting $800 billion USD, the equivalent of 10% of China’s GDP in 2014, directly into China’s primary stock market, the Shanghai Index in order to keep the bubble inflated. A six-month trading halt for 1,400 companies operating on the stock market was implemented concurrently. This massive state intervention was intended to stabilise the market at 4,600 points. Its comprehensive failure resulted in a rout.

On July 15, China’s National Bureau of Statistics announced 7% GDP growth in the second quarter of the year, in line with Li’s growth target for 2015 and China’s 7.4% in 2014. However, this too failed to boost consumer confidence, with the Shanghai Index falling 8.5% on July 27 to 3,700 index points.

In desperation, on August 11, China controversially devalued its currency to a three-year low. In a single day the Yuan lost 1.9% of its value, followed by a further 1% decline on 12 August. The move by the Chinese central bank had a detrimental effect on regional Asian stock markets and global financial markets. In New York and London, billions were wiped off the value of shares and currencies amid cries from Washington that China was launching a currency war.

The worst was yet to come for Chinese shareholders. On August 24, China’s financial markets endured their biggest one-day fall since 2007, with the Shanghai Index dropping 600 points to finish below 3,200 index points. The Chinese state broadcaster Xinhua, which had played down economic concerns in previous weeks, termed the day ‘Black Monday‘, a phrase repeated in Western media outlets. In just three months between June 12 and August 24, the entire financial gains of 2015, totalling an astounding $5.5 trillion USD, were wiped out, thousands of Chinese had lost their savings and international confidence in China was shaken.

The Communist Party’s worst fears

For a period of several weeks, the world saw a glimpse of the Chinese Communist Party’s worst nightmare. An economic crisis driven by inexorable market forces that, in spite of a massive state intervention by the Chinese central bank, continued to its bloody conclusion. For Beijing to have overseen a stock market slump in which hundreds of thousands of lower and middle income Chinese citizens lost their savings was a disaster in terms of Beijing’s economic legitimacy.

In the days that followed ‘Black Monday’, questions began to be asked in the West over Li Keqiang’s future. Under his stewardship, the certainty China’s economic rise has enjoyed for the past three decades has been undermined.

Li, however, is too high-profile a figure for Xi Jinping to remove outright, and too important for the factional equilibrium within the CCP hierarchy. Instead, in the last few months the government has provided scapegoats for the ‘Great Fall of China’. Journalist Wang Xiaolu from China’s equivalent of the Financial Times was forced to make an on-air confession that his reporting aided the collapse of the Shanghai Index. Executives from brokerage firm Citic Securities were also detained, as were employees from the regulatory commission.

The role played by China’s stock market is smaller in the context of the overall Chinese economy than in the West. However, the stock market collapse combined with the massive explosions in Tianjin on August 12, challenge the narrative that CCP governance is contiguous with stability and security. The massive rescue package and currency devaluation saw a collision between the political and the economic and it appeared both domestically and internationally that the CCP fears an economic slowdown. In a society where “saving face” is central, recent events have seen Beijing humiliated.

The question the “Great Fall of China” raises concerns about the CCP’s reaction to a hypothetical economic shock to a larger sector of the Chinese economy, such as manufacturing. How would Beijing react if, millions, instead of thousands of Chinese citizens’ economic security was suddenly called into question? How would the usually compliant, but aspirant middle class react to a sudden crisis in living standards? What would happen if, as we witnessed in Tianjin, multiple events combine to encapsulate to the public the failure of legitimacy of the central government? Would we once again see a turn to legitimacy via the People’s Liberation Army? Since 1989, this is the scenario all Chinese leaders have sought to avoid. The ‘Great Fall of China’ has revealed not just what China dreams, but also what lies within its nightmares.

{kind=link}