July 1st marked Somalia’s 55th Independence Day and the unfortunate reality that much of its freedom from oppressive colonization consisted of decades under a dictatorship and a crippling civil war. The Somali Civil War, beginning in 1991 with the overthrowing of the Barre regime, resulted in the absence of a central government and the nation’s being characterized as a ‘failed state’. It was not until 2012 that a permanent government was established and the long road towards recovery began. Somalia is now considered a ‘fragile state’ as it battles against poverty and continuing violence inflicted by the terrorist group Al-Shabaab.

July 1st marked Somalia’s 55th Independence Day and the unfortunate reality that much of its freedom from oppressive colonization consisted of decades under a dictatorship and a crippling civil war. The Somali Civil War, beginning in 1991 with the overthrowing of the Barre regime, resulted in the absence of a central government and the nation’s being characterized as a ‘failed state’. It was not until 2012 that a permanent government was established and the long road towards recovery began. Somalia is now considered a ‘fragile state’ as it battles against poverty and continuing violence inflicted by the terrorist group Al-Shabaab.

Somalia has lacked any formal banking service since the collapse of the government, a situation that allowed many informal money transfer operators to arise and fill the void. The conflict severely restricted the development of the banking system and its infrastructure, with the country’s first automated teller machines being installed only last year in the capital, Mogadishu. Its progress continues with the announcement at the June World Economic Forum on Africa, that MasterCard will be the first international banking institution to enter Somalia. It is the last African market, aside from nations under sanctions, where MasterCard is not present. Somalia’s Minister of Planning and International Cooperation called the partnership a “historic milestone, signalling Somalia’s financial liberation following years of being excluded from participating in the global economy,”

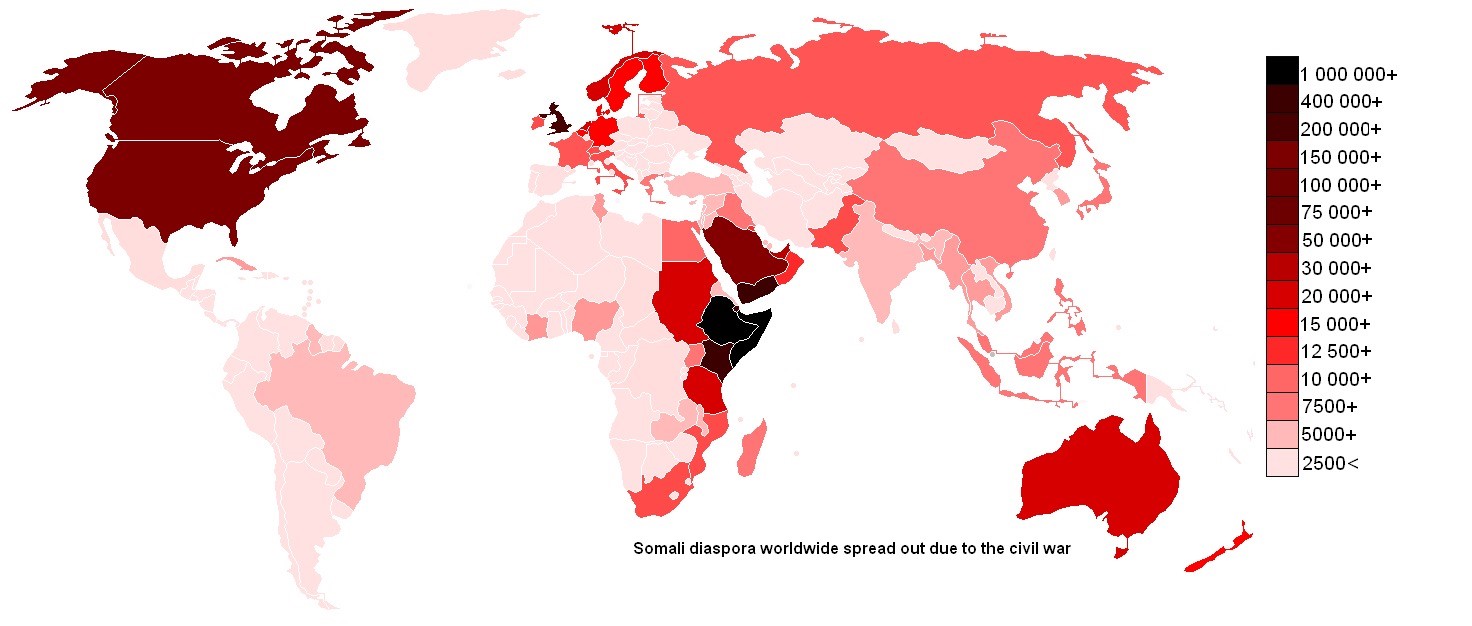

With much of the country’s population living in poverty, families and businesses are heavily reliant on financial transfers from the vast diaspora community, known as remittances. Somalis send more than $1.3 billion in remittances to friends and relatives, which account for over 35% of GDP and half of the country’s annual income. More money is sent through these remittances than is received from humanitarian aid, thereby serving to further the nation’s development as well as reducing its dependence on foreign aid. The bulk of the money is used for food, clothing, and medicine and in times of distress, such as the 2011 drought and flood, have been a lifeline crucial to many people’s survival.

2011 East Africa Drought

International remittances sent via mobile technology accounted for less than 2 percent of remittance flows in 2013, as most Somali immigrants use an informal banking system called hawala. In the hawala system, both unreliable and difficult to regulate, money is transferred via a network of hawala brokers and is defined as ‘the transfer of money without actually moving it’. The lack of transparency discourages many banks, for fear of being inadvertently involved in money laundering or terrorist financing, specifically in supporting Al-Shabaab. In January, 2015 the Merchants Bank of California, handling between 60 percent and 80 percent of all U.S. transfers to Somalia, announced that it would shut down after a federal government crackdown on money laundering. Suspicions of terrorist financing increased with the April Al-Shabaab attack on a neighbouring Kenyan University, leaving nearly 150 dead, which forced the Kenyan government to freeze the accounts of Somali banks and hawala money transfer services.

Somali Worldwide Diaspora

The situation has left many Somalis struggling to access much needed remittances from friends and relatives abroad, thereby creating a billion dollar gap that MasterCard is seeking to fill. MasterCard Inc. is linking up with Somalia’s Premier Bank to issue debit cards, with 5,000 cards targeted for 2015. Distinct from the hawala system, MasterCard constitutes a formal, traceable network that complies with international security standards. This is significant for Somali immigrants and international aid organizations, who can now send funds without the risk of transferring and transporting cash.

“If the country’s not under sanctions, it’s open for business,” said MasterCard’s division president for sub-Saharan Africa. Approximately 80 to 90 percent of transactions on the African continent are still done in cash only, leaving a massive market for MasterCard and Visa to fight over and stake their claims in. However, the situation is beneficial to both sides as the introduction of a formal banking system and companies like MasterCard “can encourage international investors to come into Somalia in a big way and contribute to the revival of the economy”.

The continuous flow of capital is all the more pertinent as a recent development within rating agencies now allows for remittances to be accounted in country credit ratings. Furthermore, the future inflows of remittances can be used as collateral to facilitate international borrowings by national banks in developing countries. The strategy of financially blockading Somalia to curb terrorist financing is counterintuitive, with insurgent organizations like Al-Shabaab using money and resources as incentives in attracting new recruits. Remittances from family abroad serve to limit the appeal of such groups, and the recent attacks show why we must make it easier to send verified humanitarian aid to countries like Somalia, not harder.

{kind=link}